Financial Resources Formulary: Unterschied zwischen den Versionen

| (10 dazwischenliegende Versionen desselben Benutzers werden nicht angezeigt) | |||

| Zeile 5: | Zeile 5: | ||

== Present values, perpetuities and annuities == | == Present values, perpetuities and annuities == | ||

'''Present value PV:''' value of a future payment C<sub>t</sub> (in year t), discounted to year 0: [[Datei: | '''Present value PV:''' value of a future payment C<sub>t</sub> (in year t), discounted to year 0: [[Datei:Form_PV.png]] | ||

'''Future value FV<sub>t</sub>:''' value of a present payment (in year 0), calculated by compounding to year t: [[Datei: | '''Future value FV<sub>t</sub>:''' value of a present payment (in year 0), calculated by compounding to year t: [[Datei:Form_FV.png]]<br/> | ||

: t year<br/> | : t year<br/> | ||

: r [[Kalkulationszinssatz|discount rate]] (interest rate)<br/> | : r [[Kalkulationszinssatz|discount rate]] (interest rate)<br/> | ||

| Zeile 38: | Zeile 38: | ||

'''Profitability index:''' ratio of NPV to investment of a project: [[Datei:Form_PI.png]] | '''Profitability index:''' ratio of NPV to investment of a project: [[Datei:Form_PI.png]] | ||

'''Equivalent annual cash flow (EAC):''' cash flow per year with the same present value as the actual cash flow of the project: [[Datei: | '''Equivalent annual cash flow (EAC):''' cash flow per year with the same present value as the actual cash flow of the project: [[Datei:cw_EAC.png]] | ||

== Interest and discount rates == | == Interest and discount rates == | ||

| Zeile 49: | Zeile 47: | ||

:- EAR for a daily rate d: EAR = (1+d)<sup>360</sup> – 1 (for 360 days per year) | :- EAR for a daily rate d: EAR = (1+d)<sup>360</sup> – 1 (for 360 days per year) | ||

Given an annual percentage rate (APR) of r, the corresponding EAR with respect to n shorter periods of equal length is: [[Datei:Form_EAR.png]] | |||

'''Effective annual rate with continuous compounding:''' effective annual rate for n → ∞ shorter periods: [[Datei:Form_EAR_cc.png]] (being r the simple annual rate) | |||

'''Annual percentage rate (APR) or simple rate:''' annualized rate of shorter period interest rates (monthly, daily rates) using simple interest. | '''Annual percentage rate (APR) or simple rate:''' annualized rate of shorter period interest rates (monthly, daily rates) using simple interest. | ||

:- APR for a monthly rate m: APR = 12 * m | :- APR for a monthly rate m: APR = 12 * m | ||

'''Real rate of return:''' rate of return adjusted for inflation: [[Datei:Form_Real_Int_1.png]] | '''Real rate of return:''' rate of return adjusted for inflation: [[Datei:Form_Real_Int_1.png]] | ||

| Zeile 65: | Zeile 63: | ||

== Valuing bonds == | == Valuing bonds == | ||

'''Price of a bond:''' [[Datei:Form_PV_Bond.png]] | '''Price of a bond:''' [[Datei:Form_PV_Bond.png]]<br/> | ||

with<br/> | with<br/> | ||

: C<sub>t</sub> annual coupon interest payment<br/> | : C<sub>t</sub> annual coupon interest payment<br/> | ||

| Zeile 84: | Zeile 80: | ||

'''(Expected) [[Wertpapierrendite|Stock return r]] (equity cost of capital):''' [[Datei:Form_Stock_Return.png]] | '''(Expected) [[Wertpapierrendite|Stock return r]] (equity cost of capital):''' [[Datei:Form_Stock_Return.png]] | ||

'''Stock price P<sub>0</sub> in the single-period case:''' [[Datei:Form_P0_einperiodig.png]] | * '''Stock price P<sub>0</sub> in the single-period case:''' [[Datei:Form_P0_einperiodig.png]] | ||

'''Dividend discount model''' for the stock price P0 in the multi-period case until time horizon H: [[Datei: | * '''Dividend discount model''' for the stock price P0 in the multi-period case until time horizon H: [[Datei:cw_DDM_v2.png]] | ||

'''Stock price P<sub>0</sub>''' with specific dividends until time horizon H and growing dividends after H: [[Datei:Form_P0_growth.png]] | * '''Stock price P<sub>0</sub>''' with specific dividends until time horizon H and growing dividends after H: [[Datei:Form_P0_growth.png]] | ||

'''Stock price for a perpetual stream of dividends:''' [[Datei:Form_P0_perpetual.png]] | * '''Stock price for a perpetual stream of dividends:''' [[Datei:Form_P0_perpetual.png]] | ||

'''Stock price for a perpetual stream of growing dividends:''' [[Datei:Form_P0_perp_growth.png]] | * '''Stock price for a perpetual stream of growing dividends:''' [[Datei:Form_P0_perp_growth.png]] | ||

* '''Stock price = Discounted earnings + growth opportunities:''' [[Datei:Cw_PVGO.png]] | |||

'''Present value of growth opportunities (PVGO):''' net present value of a firm's future investments. | |||

'''Return (Equity cost of capital) of a perpetual stream of dividends with growth:''' [[Datei:Form_RoE_growth.png]] | '''Return (Equity cost of capital) of a perpetual stream of dividends with growth:''' [[Datei:Form_RoE_growth.png]] | ||

| Zeile 101: | Zeile 102: | ||

'''Plowback ratio:''' fraction of earnings retained by the firm: [[Datei:Form_Plowback.png]] | '''Plowback ratio:''' fraction of earnings retained by the firm: [[Datei:Form_Plowback.png]] | ||

'''Sustainable growth rate:''' rate at which a firm can steadily grow: [[Datei:Form_Sustainable.png]] | '''Sustainable growth rate:''' rate at which a firm can steadily grow: [[Datei:Form_Sustainable.png]] | ||

| Zeile 110: | Zeile 109: | ||

== Risk and return == | == Risk and return == | ||

'''Risk premium of an asset:''' asset return – return of risk-free asset | '''Risk premium of an asset:''' asset return – return of risk-free asset. | ||

'''Variance:''' expected value of squared deviations of observations from their expected value (mean): [[Datei:Form_Var.png]] (based on j observations) | |||

'''Standard deviation:''' a measure of volatility of expected stock returns: [[Datei:Form_Standard_Dev.png]] | |||

'''Expected portfolio return''' (with two assets): | '''Expected portfolio return''' (with two assets): [[Datei:Form_EV_zwei.png]] | ||

'''Expected portfolio return''' (with j = 1, …, n assets): | '''Expected portfolio return''' (with j = 1, …, n assets): [[Datei:Form_EV_n.png]] | ||

:x<sub>j</sub> weight of asset j in the portfolio<br/> | :x<sub>j</sub> weight of asset j in the portfolio<br/> | ||

| Zeile 128: | Zeile 123: | ||

:r<sub>j</sub> (expected) return of asset j<br/> | :r<sub>j</sub> (expected) return of asset j<br/> | ||

'''Variance of portfolio return (portfolio variance)''' in the case of two assets: | '''Variance of portfolio return (portfolio variance)''' in the case of two assets: [[Datei:Form_Port_Var_zwei.png]] | ||

'''Covariance''' between asset i and j with | '''Covariance''' between asset i and j with [[Datei:Form_Covariance_Formel.png]] | ||

'''Correlation coefficient''' between asset i and j: | '''Correlation coefficient''' between asset i and j: [[Datei:Form_Corr_Coeff_Formel.png]] | ||

'''Variance of portfolio return (portfolio variance)''' in the case of n assets: | '''Variance of portfolio return (portfolio variance)''' in the case of n assets: [[Datei:Form_Port_Var_n.png]] | ||

'''Sharpe-Ratio: ratio of risk premium to risk (standard deviation): [[Datei:cw_Sharpe_ratio.png]] | |||

'''Beta''' of the return of asset j to the market return (return of market portfolio m): | '''Beta''' of the return of asset j to the market return (return of market portfolio m): [[Datei:Form_Beta.png]] | ||

'''Expected return following the security market line''' equation (SML): | '''Expected return following the security market line''' equation (SML): [[Datei:Form_Expected_Return.png]] | ||

Expected return of a stock in '''event studies''': | Expected return of a stock in '''event studies''': [[Datei:Form_Normal_Return.png]] | ||

'''Abnormal return''' = actual return – expected return = | '''Abnormal return''' = actual return – expected return = [[Datei:Form_Abnormal.png]] | ||

== Capital Structure and Return == | == Capital Structure and Return == | ||

'''[[Rentabilität|Rates of return]]:''' | '''[[Rentabilität|Rates of return]]:'''<br/> | ||

[[Datei:Form_RoI.png]]<br/> | |||

[[Datei:Form_RoA.png]]<br/> | |||

[[Datei:Form_RoC.png]] | |||

'''Weighted average cost of capital (WACC):''' [[Datei:Form_WACC_after_Tax.png]] | |||

'''Weighted average cost of capital (WACC):''' | |||

:r<sub>D</sub> interest rate on debt resp. debt cost of capital | :r<sub>D</sub> interest rate on debt resp. debt cost of capital | ||

| Zeile 163: | Zeile 157: | ||

:T<sub>c</sub> corporate tax rate | :T<sub>c</sub> corporate tax rate | ||

'''Weighted average cost of capital (WACC)''' with a zero-tax rate: | '''Weighted average cost of capital (WACC)''' with a zero-tax rate: [[Datei:Form_WACC.png]] | ||

'''Leverage-formula''' for return on equity: return on equity increases with debt/equity-ratio | '''Leverage-formula''' for return on equity: return on equity increases with debt/equity-ratio: [[Datei:Form_Leverage.png]] | ||

'''Leverage-formula''' for equity beta: risk increases with debt/equity-ratio: [[Datei:Form_Leverage_Beta.png]] | |||

== Exercises == | |||

Please try our [[Financial Exercises]] or have a look at the [[Financial Ratios]] or at our [[Investition|investment pages]].<br/> | |||

Aktuelle Version vom 14. Mai 2012, 11:08 Uhr

by Clemens Werkmeister

Present values, perpetuities and annuities

Present value PV: value of a future payment Ct (in year t), discounted to year 0: ![]()

Future value FVt: value of a present payment (in year 0), calculated by compounding to year t: ![]()

- t year

- r discount rate (interest rate)

discount factor with discount rate (interest rate) r for t years

discount factor with discount rate (interest rate) r for t years- Ct cash flow in year t

- C0 initial investment of a project (for normal investment projects: C0 < 0)

- T number of years of the project

The sum of several present values is a PV, too (additivity of present values):![]()

Net present value NPV: PV of future payments (of a project or a company) plus the - usually negative - initial investment C0: ![]()

Perpetuity (console): a periodic (annual) payment C that is received or paid forever (beginning with the first payment at the end of year 1):![]()

Annuity: a payment of a level cash flow C during a specified number of years (from year 1 to n). Its present value can be calculated as difference between two perpetuities: ![]()

Annuity (recovery) factor: average payment at the end of n periods, corresponding to a present value PV and considering for interest rate r:![]()

Annuity present value factor: factor for the PV of n equal payments at the end of years 1 to n: ![]()

The annuity C for years 1 to n corresponding to a present value PV and discount rate r is: ![]()

Growing perpetuity: a perpetuity starting with cash flow C1 in year 1 and increasing by the annual growth rate g forever:![]() (for t = 1, 2, …, ∞ ;g < r) and

(for t = 1, 2, …, ∞ ;g < r) and ![]()

Growing annuity: an annuity starting with cash flow C1 in year 1 and increasing by the annual growth rate g for n years: ![]() (with t = 1, 2, …, n)

(with t = 1, 2, …, n)

Internal rate of return (IRR): discount rate that results in NPV = 0: ![]()

Profitability index: ratio of NPV to investment of a project: ![]()

Equivalent annual cash flow (EAC): cash flow per year with the same present value as the actual cash flow of the project:

Interest and discount rates

Effective annual rate (EAR): annualized rate of shorter period interest rates (monthly, daily rates) using compound interest:

- - EAR for a monthly rate m: EAR = (1+m)12 – 1

- - EAR for a daily rate d: EAR = (1+d)360 – 1 (for 360 days per year)

Given an annual percentage rate (APR) of r, the corresponding EAR with respect to n shorter periods of equal length is: ![]()

Effective annual rate with continuous compounding: effective annual rate for n → ∞ shorter periods: ![]() (being r the simple annual rate)

(being r the simple annual rate)

Annual percentage rate (APR) or simple rate: annualized rate of shorter period interest rates (monthly, daily rates) using simple interest.

- - APR for a monthly rate m: APR = 12 * m

Real rate of return: rate of return adjusted for inflation: ![]() →

→ ![]() (being i the inflation rate)

(being i the inflation rate)

Valuing bonds

Price of a bond: ![]()

with

- Ct annual coupon interest payment

- F face value (or principal)

- r discount rate (yield to maturity)

- N maturity

Duration of a bond with maturity N: weighted average period of bond payments:

Modified duration: a measure of volatility (elasticity) of bond prices: ![]()

Valuing stocks

(Expected) Stock return r (equity cost of capital): ![]()

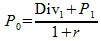

- Stock price P0 in the single-period case:

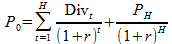

- Dividend discount model for the stock price P0 in the multi-period case until time horizon H:

- Stock price P0 with specific dividends until time horizon H and growing dividends after H:

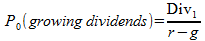

- Stock price for a perpetual stream of dividends:

- Stock price for a perpetual stream of growing dividends:

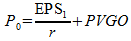

- Stock price = Discounted earnings + growth opportunities:

Present value of growth opportunities (PVGO): net present value of a firm's future investments.

Return (Equity cost of capital) of a perpetual stream of dividends with growth: ![]()

Return on Equity with market values: ![]()

Payout ratio: fraction of earnings paid out as dividends: ![]()

Plowback ratio: fraction of earnings retained by the firm: ![]()

Sustainable growth rate: rate at which a firm can steadily grow:

Discounted cash flow (DCF): value of the free cash flows that are available to investors plus company value at the planning horizon, all discounted to present: ![]()

Risk and return

Risk premium of an asset: asset return – return of risk-free asset.

Variance: expected value of squared deviations of observations from their expected value (mean): ![]() (based on j observations)

(based on j observations)

Standard deviation: a measure of volatility of expected stock returns: ![]()

Expected portfolio return (with two assets): ![]()

Expected portfolio return (with j = 1, …, n assets): ![]()

- xj weight of asset j in the portfolio

- rj (expected) return of asset j

Variance of portfolio return (portfolio variance) in the case of two assets: ![]()

Covariance between asset i and j with ![]()

Correlation coefficient between asset i and j: ![]()

Variance of portfolio return (portfolio variance) in the case of n assets: ![]()

Sharpe-Ratio: ratio of risk premium to risk (standard deviation): ![]()

Beta of the return of asset j to the market return (return of market portfolio m): ![]()

Expected return following the security market line equation (SML): ![]()

Expected return of a stock in event studies: ![]()

Abnormal return = actual return – expected return = ![]()

Capital Structure and Return

Weighted average cost of capital (WACC): ![]()

- rD interest rate on debt resp. debt cost of capital

- rE return on equity resp. equity cost of capital

- Tc corporate tax rate

Weighted average cost of capital (WACC) with a zero-tax rate: ![]()

Leverage-formula for return on equity: return on equity increases with debt/equity-ratio: ![]()

Leverage-formula for equity beta: risk increases with debt/equity-ratio: ![]()

Exercises

Please try our Financial Exercises or have a look at the Financial Ratios or at our investment pages.